For discussion purposes only, I have attached a redacted snapshot taken from part of a recent Form 8-K that was filed with the SEC. I have no personal information about or involvement in the situation. This post is only for discussion purposes. Unfortunately news or developments today tend to be assumed or characterized to be in the negative, and often so assumed immediately and long before the facts are investigated, evaluated and made available. It takes a while to do a full investigation and to then evaluate what is known, what is not yet known, and what might not ever be known, within the context of the law and the certainty and uncertainty that exists, etc. People are innocent and presumed to be innocent and not at fault unless and until proven otherwise by admissible evidence.

Whoever is doing an investigation must be sufficiently qualified and sufficiently independent of the situation, including consideration of possible relevant personal, family, social or other outside relationships. The qualifications and independence become more elevated if the alleged situation and subject matter at issue possibly evidence greater exposure or reach into higher levels of management and authority.

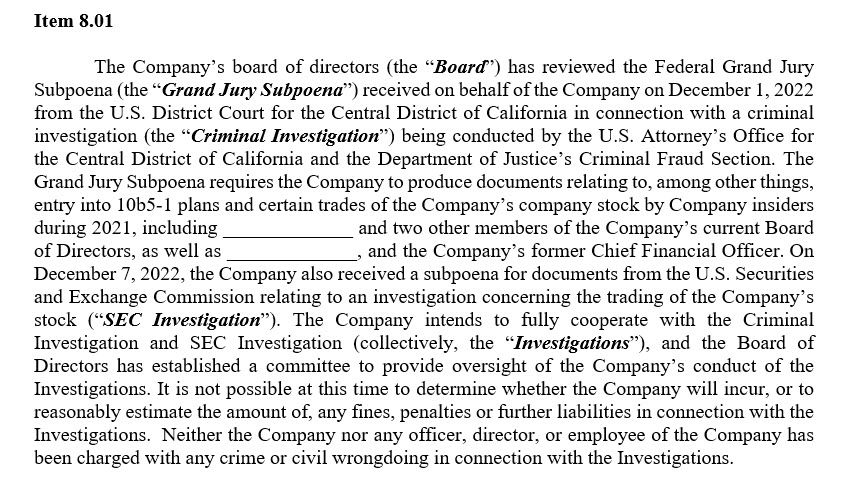

Item 8.01 states “the Board of Directors has established a committee to provide oversight of the Company’s investigation” but no additional information is provided in that regard. Obviously as this situation is alleged to involve board and CxO members, the members of the committee that has been established must be carefully vetted. And consideration must also be given to optics, and to possible other high ranking or high status or visibility people from whom information might be sought and obtained during the investigation, possibly including, depending on the situation, other high-level management and board members, general counsel, internal and outside audit, and people who are members of a compliance function that is relevant to the situation. Obviously the Company’s compliance, internal controls and risk management processes relative to the issues involved also should be reviewed and evaluated and improved if necessary. Although not a legal issue, in circumstances where it becomes appropriate, possible impact on relationships and trust going forward also should be considered and worked on if necessary.

Outside, separate attorney representation also will be engaged and retained by multiple people and entities involved. Of course, possible sources of payment, reimbursement, or indemnification for the expense of legal counsel also must be evaluated and pursued.

You may know from some of my other materials that I am also interested in audit committees and governance committees, audit and auditing, internal controls and processes, auditing function and auditor communications with management, those involved in governance, and audit committees, CAMs, NOCLAR pronouncements that are becoming effective, and similar topics and matters.

That is all that I have in this post – as I said, I do not have personal information about or involvement in this situation, and, frankly, I could not talk about it if I did.

The following is the name redacted Item 8.01 from the form 8-K:

Thank you for reading. Please do pass this blog and blog post and information to other people who would be interested as it is only through collaboration and sharing that great things and success are more quickly achieved.

* * * * * * *

Best to you,

David Tate, Esq. (and inactive CPA)

- Business litigation and disputes – business, breach of contract/commercial, co-owners, shareholders, investors, founders, workplace and employment, environmental, D&O, governance, boards and committees.

- Trust, estate and probate court litigation and disputes – trust, estate, probate, elder and dependent abuse, conservatorship, POA, real property, mental health and care, mental capacity, undue influence, conflicts of interest, and contentious administrations.

- Governance, boards, audit and governance committees, investigations, auditing, ESG, etc.

- Mediator and facilitating dispute resolution:

- Trust, estate, probate, conservatorship, elder and dependent abuse, etc.

- Business, breach of contract/commercial, owner, shareholder, investor, etc.

- D&O, board, audit and governance committee, accountant and CPA related.

- Other: workplace and employment, environmental, trade secret.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation, or as or for my opinions and views on the subject matter.

Also note – sometimes I include links to or comments about materials from other organizations or people – if I do so, it is because I believe that the materials are worthwhile reading or viewing; however, that doesn’t mean that I don’t or might not have a different view about some or even all of the subject matter or materials, or that I necessarily agree with, or agree with everything about or relating to, that organization or person, or those materials or the subject matter.

Please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

My two blogs are:

http://tateattorney.com – business, D&O, audit committee, governance, compliance, etc. – previously at http://auditcommitteeupdate.com

Trust, estate, conservatorship, elder and elder abuse, etc. litigation and contentious administrations http://californiaestatetrust.com

David Tate, Esq. (and inactive California CPA) – practicing only as an attorney in California.